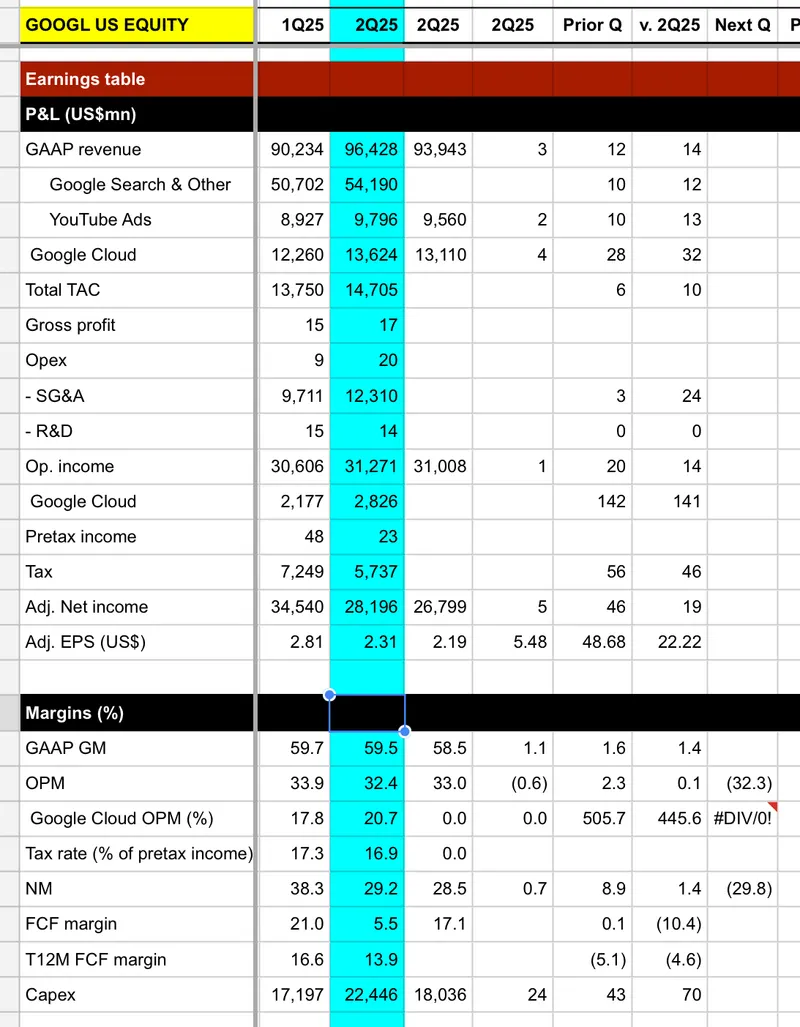

- 2Q25 EPS beat by 5% on rev/OPI were 3%/1% ahead of Street consensus. FCF margin of 5.5% was well below Street’s 17.1% => #成長不錯但整體獲利和品質有點差強人意的一季

- Search & YT Ads YoY accelerated to 12%/13% from 10%/10% in 1Q25 => #略優於預期。

- Google Cloud, the AI monetization proxy, revenue YoY accelerated to 32% from 28% in 1Q25, better than expected thanks to demand from AI. OPM improved to 20.7% => #成長和獲利都有達到前一篇做preview的高標。

- 2025 FY Capex guidance raised to US$85bn from prior US$75bn & ~US$73 expected => #這應該是為什麼一開始盤後跌了2%左右的原因,#且確實造成FCF產生狀況遠低於預期。

消化一下,晚一點開始正式對答案檢討 preview 寫的對不對。

- 2Q25 EPS beat by 5% on rev/OPI were 3%/1% ahead of Street consensus. FCF margin of 5.5% was well below Street’s 17.1% => #成長不錯但整體獲利和品質有點差強人意的一季

- Search & YT Ads YoY accelerated to 12%/13% from 10%/10% in 1Q25 => #略優於預期。

- Google Cloud, the AI monetization proxy, revenue YoY accelerated to 32% from 28% in 1Q25, better than expected thanks to demand from AI. OPM improved to 20.7% => #成長和獲利都有達到前一篇做preview的高標。

- 2025 FY Capex guidance raised to US$85bn from prior US$75bn & ~US$73 expected => #這應該是為什麼一開始盤後跌了2%左右的原因,#且確實造成FCF產生狀況遠低於預期。

消化一下,晚一點開始正式對答案檢討 preview 寫的對不對。