Introduction and Comparison of Tax Benefits Application for Foreign Companies Earning Income from Taiwan (Chapter 2)

When foreign companies earn income from Taiwan and want to reduce their tax burden, aside from the Taiwan Income Tax Act Article 25 and point 15-1 of Taiwanese sourced income guideline discussed in the previous chapter, another common tax benefit is to apply for tax benefits through tax treaties signed between the two countries.What is a Tax Treaty?

Tax treaties are agreements signed between countries/jurisdictions to avoid double taxation and prevent tax evasion. These treaties have significant impacts on multinational companies and individuals. This section will explore how to apply Article 7 (Business Profits) and Article 10 (Dividends) of tax treaties and explain the tax benefits of these articles and how they should be practically applied.

Article 7 of the Tax Treaty: Business Profits

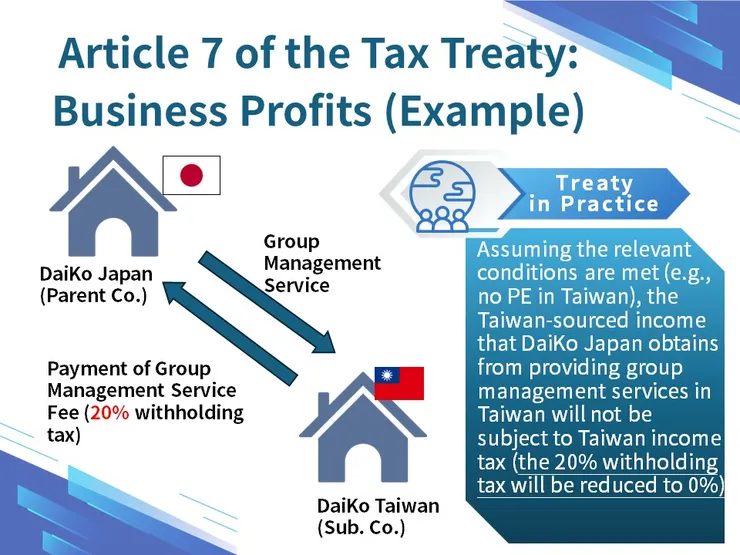

Take the tax treaty between Taiwan and Japan as an example. According to Article 7 of the Taiwan-Japan tax treaty, the profits of an enterprise of one territory are taxable only in that territory unless the enterprise carries on business in the other territory through a permanent establishment (PE) situated therein. If the enterprise carries on business as aforesaid, the profits of the enterprise may be taxed in the other territory but only so much of them as is attributable to that permanent establishment.

In simpler terms, if a multinational company does not have a permanent establishment in another country, its business profits should only be taxed in one territory (usually the home country where the multinational company is located).

Example Explanation:

DaiKo Group is a multinational company headquartered in Japan (parent company: DaiKo Japan) with a subsidiary in Taiwan (DaiKo Taiwan). To enhance group operational efficiency, DaiKo Japan provides group management services to its subsidiary annually, including formulating group operational policies, budgeting, and providing management guidance in Japan. DaiKo Taiwan pays management service fees to DaiKo Japan annually, subject to a withholding tax rate of 20%.

Assuming DaiKo Japan meets the relevant conditions (e.g., no permanent establishment in Taiwan), DaiKo Japan can apply for the tax benefits under Article 7 of the Taiwan-Japan tax treaty, meaning that the income DaiKo Japan earns from providing group management services in Taiwan will not be subject to Taiwan income tax (the 20% withholding tax will become 0%).

Of course, when applying, DaiKo Japan needs to prepare adequate documentation and evidence, such as proofs of service and income calculation methods, to substantiate the transaction as well as persuade the Taiwan tax authorities.

Article 10 of the Tax Treaty: Dividends

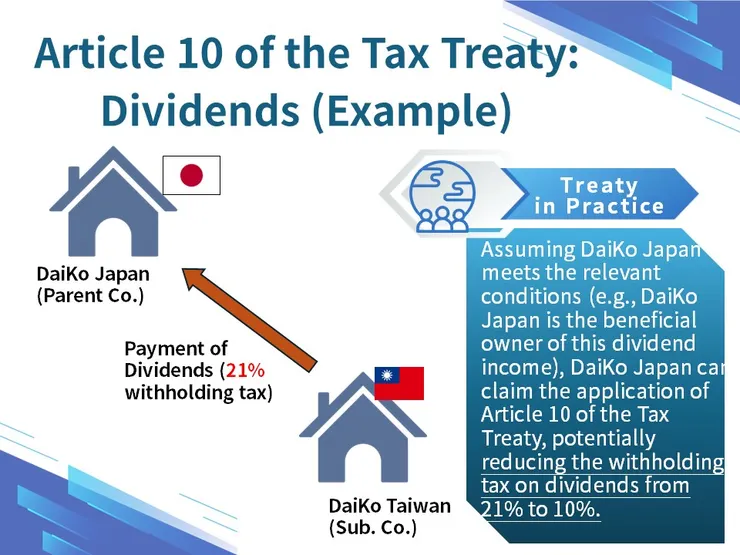

According to Article 10 of the Taiwan-Japan tax treaty, dividends paid by a company resident in one territory to a resident of the other territory may be taxed in that other territory. However, such dividends may also be taxed in the territory of the company paying the dividends according to the laws of that territory, but if the beneficial owner of the dividends is a resident of the other territory, the tax so charged shall not exceed 10% of the gross amount of the dividends.

In other words, under the Taiwan-Japan tax treaty, when one company pays dividends to another company, if the relevant conditions are met, the withholding tax on dividends should not exceed 10%.

Example Explanation:

Continuing from the previous example, DaiKo Taiwan pays dividends to DaiKo Japan annually, subject to a withholding tax rate of 21%.

Assuming DaiKo Japan meets the relevant regulations (e.g., DaiKo Japan is the beneficial owner of the dividend income), DaiKo Japan can apply for the tax benefits under Article 10 of the Taiwan-Japan tax treaty, potentially reducing the withholding tax on dividends from 21% to 10%.

Conclusion

Applying Articles 7 and 10 of tax treaties can bring significant tax benefits to multinational companies, which is crucial for their operations in the international market. However, these articles also pose practical challenges, including the identification of permanent establishments, profit attribution, and confirmation of the ultimate beneficial owner.

The application process can be quite complicated. Additionally, under the latest international tax regulations, if there are existing tax treaty benefits and the beneficiary does not actively apply for them when earning income, it may affect their rights to apply for foreign tax credits in their home country.

Therefore, companies need to thoroughly understand the relevant provisions when utilizing tax treaties. It is recommended that multinational companies work with professional tax advisors to ensure compliance and maximize tax benefits.